Azimuth

Executive Summary

The semiconductor industry leads all major critical mineral intensive manufacturing sectors – including clean energy and defense – in both profit margins and growth, fueled by AI driven demand for chips and data center infrastructure. However, this industry faces existential risk from an unpredictable supply of critical minerals and metals driven by rising geopolitical risk and single source disruption. Every layer of the semiconductor stack, from equipment to memory, depends on critical minerals procured from intensively concentrated production sources that expose semiconductor companies to multi billion-dollar revenue risk. Azimuth has launched Nexaltis Minerals, a customer led critical minerals processing platform dedicated to addressing resiliency for AI and semiconductor supply chains. Nexaltis Minerals is aggregating critical minerals demand across the full chipmaking stack and building commercial scale midstream critical minerals infrastructure.

Why Semiconductors Are the Strongest End Market for Critical Minerals

Semiconductor manufacturing generates margins that most industrial sectors cannot approach, with gross margins spanning 25% at foundries (physical chip manufacturing) to 55% and above in lithography (machines that etch circuit patterns onto silicon)[i]. The margins are protected because switching costs are enormous and qualification timelines are long, meaning customers have little choice but to pay. A modern fab costs tens of millions of dollars per day to operate at capacity. Any input shortage that stops the line is catastrophic relative to the cost of the input itself. When it comes to critical minerals, the cost of the mineral is negligible compared to production downtime.

However, the global semiconductor industry’s upstream suppliers are subject to existential global policy interventions in the form of export controls on rare earth elements (REEs), gallium, germanium, and tungsten, to name a few examples – all of which are critical for semiconductor and electronics production. For two of the most important semiconductor heavy REEs (HREEs), dysprosium and terbium, countries outside of China are expected to meet less than a fifth of demand by 2035[ii].

This dynamic makes the semiconductor supply chain the most durable end user for critical minerals. Companies qualify suppliers over years and remain sticky customers. A mineral processor that achieves semiconductor grade qualification sits in a position that is difficult to displace and nearly impossible for a late entrant to replicate quickly. Supplying the critical minerals relevant to each layer of the stack is, in that sense, closer to contracted infrastructure than to commodity supply

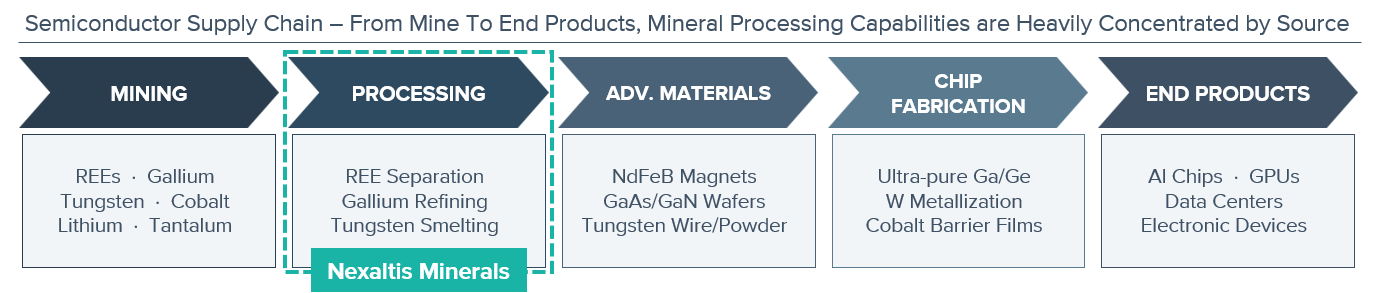

Critical Mineral Demand Across the Semiconductor Stack

The type and form factor of critical minerals for semiconductor and electronics supply chains depends on the use case. Each layer demands specific inputs tied to its core processes, and for the majority of those inputs, processing capacity is concentrated in a handful of countries, creating a structural dependency that Western supply chains have only started to address. Below is a description of players tied to each layer of the global semiconductor supply stack, from those closest to raw materials, such as the equipment makers and subsystems (tools and specialty chemicals) to the downstream memory companies that drive their metals procurement cycle.

Equipment. The world’s leading equipment makers supply deposition and etching tools to every fab. These systems require tungsten for hard coatings and contact layers and HREEs including dysprosium and terbium for the high-performance magnets in their motors and actuators.

Subsystems and Component Suppliers. These companies produce lasers, optics, process control systems, and vacuum components for buyers across the entire semiconductor stack. Gallium and germanium are essential for compound semiconductor lasers and infrared optics. HREEs such as gadolinium are used in logic chips and memory devices, and magnetic materials such as terbium and dysprosium are used in electronic applications.

Lithography. Extreme ultraviolet (EUV) systems – the only commercially viable technology for sub-5nm logic manufacturing – depend on dysprosium for magnet systems and tin for the EUV plasma source. This industry has one primary supplier, thus customers face prohibitively high near-term switching costs, but this supplier is simultaneously dependent on hard-to-source minerals.

Foundries. These companies deploy gallium-based processes in advanced packaging and compound semiconductor lines. Gallium nitride and gallium arsenide are central to the radio frequency and power devices that AI hardware increasingly requires.

Memory. These companies produce memory chips that rapidly store and retrieve information to perform billions of calculations that enable data to be processed and consumed in mobile devices, server farms, and today’s growing AI applications.[iii]. Tungsten interconnects run through every memory device. Germanium is used in phase change memory and advanced node processes.

Why the Industry Cannot Solve This Alone: Nexaltis Minerals

The semiconductor industry’s critical mineral exposure is well understood across the value chain. However, individual buyers, including equipment makers, memory producers, and logic foundries, require volumes too small to justify the capital to anchor a singular, dedicated processing project on their own. The reward for solving the critical mineral supply chain benefits the entire industry, but the bill cannot fall on individual actors.

A demand aggregation market mechanism is an option to service the critical mineral needs of the semiconductor industry. By assembling offtake of critical minerals spanning the full stack of equipment makers, subsystem suppliers, foundries, and memory producers, the volume needed to anchor a Western processing project becomes accessible. With contracted offtake, a critical minerals processing project becomes bankable. The coalition approach distributes the commitment across buyers who collectively have far more ability to anchor a processing project.

Nexaltis Minerals is Azimuth’s development company built to serve as a critical minerals processing platform to produce semiconductor and electronics grade materials with a North America-led vertically integrated approach. Nexaltis Minerals sources advantaged feedstocks and established processing needed to convert those feedstocks into high value mineral products. Extensive customer conversations have shown the semiconductor industry to be highly collaborative and demand for a platform like Nexaltis Minerals is strong. Nexaltis is positioned to play a central role in providing resilient critical mineral supply chains over the next decade.